Automation in Banking and Finance

The real challenge banks and credit unions face is determining when to start their automation journey. The privacy and security of information collected and stored by financial services providers is of the highest priority. Numerous solutions exist to help organizations extract data from documents for use throughout loan origination and new account opening processes.

For this reason, robotic process automation (RPA), or using bots to perform these recurring tasks, is also gaining steam across the industry. Rather than replace human staff and lose many institutions’ key differentiator – their relationship-first service – a strategic approach to automation aims to make work for banking staff more meaningful and impactful. Business processes like account closing, dispute tracking and rate changes are vital, but they shouldn’t monopolize internal resources like brain power, time and dollars. With the proper use of automation, customers can get what they need quicker, employees can spend time on more valuable tasks and institutions can mitigate the risk of human error. By automating tedious, repetitive tasks, employees can focus on ones that require complex thought or interpersonal skills. A bank can now select from cream-of-the-crop providers and deploy within days.

This consistently increases productivity, further enhancing customer satisfaction. This means automated cash management is beneficial for customers and team members, improving employee morale. Branch automation can also streamline routine transactions, giving human tellers more time to focus on helping customers with complex needs. This leads to a faster, more pleasant and more satisfying experience for both teller and customer, as well as reducing inconvenience for other customers waiting to speak to the teller.

Supporting the Future

Centralizing data in a single source through automated facility management software serves as one big step in the process. Since each bank’s projects may vary, requiring the standardization of operating procedures and adoption of service-level agreements will keep these transformations efficient despite their individual challenges. Banks used to manually construct and manage their accounting and loan transaction processing before computerized systems and the internet.

- The digital world has a lot to teach banks, and they must become really agile.

- Current asset transactions are being replicated on the Blockchain as part of industry trials of the technology.

- Banks now have a window of opportunity to influence customer preferences, create a renewed culture of innovation and opportunity, increase customer loyalty, and strengthen human relationships.

- Branch automation with cash management should be an integral part of any financial institution.

Automating cash processes using cash deposit and recycling solutions, provides banks with many benefits. MX8800

Maximize client satisfaction and branch productivity with the next generation of secure, customer-centric branch transformation platforms from Nautilus Hyosung. The MX8800 streamlines branch transactions and secure autonomously or with assistance of branch staff. Your customers are increasingly more comfortable with self-service banking via their smartphone, tablet or PC and we have the solutions to increase automation. Bancsource partners with Nautilus Hyosung to deliver relevant, state of the art, technologies to our customers.

Let’s talk solutions.

AVS “checks the billing address given by the card user against the cardholder’s billing address on record at the issuing bank” to identify unusual transactions and prevent fraud. Financial technology firms are frequently involved in cash inflows and outflows. The repetitive operation of drafting purchase orders for various clients, forwarding them, and receiving approval are not only tedious but also prone to errors if done manually. For banks, overcoming legacy systems, and rethinking how they have done things for the last several decades, won’t be an overnight change. This will be a step-by-step approach that will require several iterations as FIs work to get it right. However, he noted, it is a necessary journey, as the market continues to evolve.

While RPA is much less resource-demanding than the majority of other automation solutions, the IT department’s buy-in remains crucial. That is why banks need C-executives to get support from IT personnel as early as possible. In many cases, assembling a team of existing IT employees that will be dedicated solely to the RPA implementation is crucial.

New Customer Onboarding Workflow

Any machine can host any software because it is the installed software that will determine the purpose of a machine; ATM, ITM, ASK, VTM. Julia Kagan is a financial/consumer journalist and former senior editor, personal finance, of Investopedia.

While larger financial conglomerates are investing big bucks in strategic automation initiatives, many smaller banks are still at the beginning of their digital transformation journey. How can community bankers gain a foothold when it seems like the competition is already well into the race? These seven insights will reveal the fundamental trends influencing banking automation decision makers. Oracle Banking Branch helps reinvent the bank branch from a point of service to a point of sale and advice.

Operate in a seamless digital banking environment with the use of banking technology

Automation solves short-term inefficiencies that can lead to long-term results, even if there is a learning curve in the start-up phase. The intended outcome is to future-proof operations and deliver meaningful results to the bottom line. “Our cash recyclers and terminals bridge the gap between the physical and digital worlds and guarantee you the highest level of reliability.” Whether your challenge needs a quick fix or a complex solution, our team is here to help.

Stearns Bank partners with FinTech Automation – ThePaypers – The Paypers

Stearns Bank partners with FinTech Automation – ThePaypers.

Posted: Mon, 23 Oct 2023 11:06:00 GMT [source]

While most consumers rely on online or digital banking, branches are still relevant. How you maintain and grow that relevance for consumers who require in-branch services is critical. New strategies and technologies are driving branch transformations that aim to improve the customer experience while lowering branch costs. As we continue to watch bank branches transform, facility teams need to change their processes at the same rate—or even faster.

During the pandemic, one area that is getting closer scrutiny is the branch network. In this era of social distancing, customers want to avoid branch visits when they can and wish to minimize time and human contact in the branch when they can’t. Plus, banks are keenly aware that they need to reduce operational costs as far as they can because of compressed fees and the possibility of rising credit defaults during the COVID-19 crisis. In recent years, the push to provide a more seamless customer experience online and offline – as well as the search for better operational efficiency – have led to a clear trend for branch transformation.

GoTyme Bank sets gold standard for customer service – Manila Bulletin

GoTyme Bank sets gold standard for customer service.

Posted: Mon, 30 Oct 2023 02:37:22 GMT [source]

By shifting the responsibility of these mundane tasks over to a machine, you can speed up processing times of notoriously protracted functions like mortgage and credit card applications. The financial services industry is changing at an ever-accelerated rate because innovation is empowering startups and disruptors to win business from traditional financial institutions. CGD is the oldest and the largest financial institution in Portugal with an international presence in 17 countries. Like many other old multinational financial institutions, CGD realized that it needed to catch up with the digital transformation, but struggled to do so due to the inflexibility of its legacy systems. When it comes to RPA implementation in such a big organization with many departments, establishing an RPA center of excellence (CoE) is the right choice. To prove RPA feasibility, after creating the CoE, CGD started with the automation of simple back-office tasks.

Namely, you’ll be in a position to serve the types of attractive online experiences that expand your customer base. Seamless self-service tools for opening accounts online and the ability for users to share transaction data with third-party apps are just some of the benefits made possible by the automation revolution. What starts as a cost-saving measure explodes into a new buffet of growth opportunities for innovative bankers. Intelligent document processing (IDP) solutions connect these internal systems to allow employees to work inside a single tool. This streamlined workflow can dramatically improve employee productivity and increase customer satisfaction, saving banks significant time and money.

Banking automation can automate the process by reviewing and reconciling data at each step and procedure, requiring minimal human participation to incorporate the essential parts of these activities. Only when the data shows, misalignments do human involvement become necessary. Banking customers want their queries resolved quickly with a touch of personalization. For that, the customers are willing to interact with automated bots and systems too. For the best chance of success, start your technological transition in areas less adverse to change. Employees in that area should be eager for the change, or at least open-minded.

The CJD 6000 is a chequebook printing machine ideally installed at every bank branch’s back office or at a centralised hub. It is uniquely designed to print fully personalised chequebooks on-demand, and can also be integrated to your electronic and mobile banking platforms to receive order requests directly from customers. RITECH particularly understands the needs of banks in the area of cheque printing, handling and processing. Our range of solutions for branch automation have helped banks around the world meet increasing customer demands as well as regulatory requirements.

It is uniquely designed to print fully personalised chequebooks on-demand, and can also be integrated to your electronic and mobile banking platforms to receive order requests directly from customers. “These bots are entering information into the core banking system around fraud alerts,” Johnston explains. “They’re putting notes into our customer relationship management systems around payments or transfers that processed with addresses that changed and a whole bunch of other things. Our robots even post about promotions, anniversaries, and birthdays on our corporate intranet.” Since starting with UiPath in 2017, Heritage has successfully automated about 80 customer-facing, back-office, and middle-office processes. These processes are spread across operations, payments, financial crimes, and contact center services, among other areas.

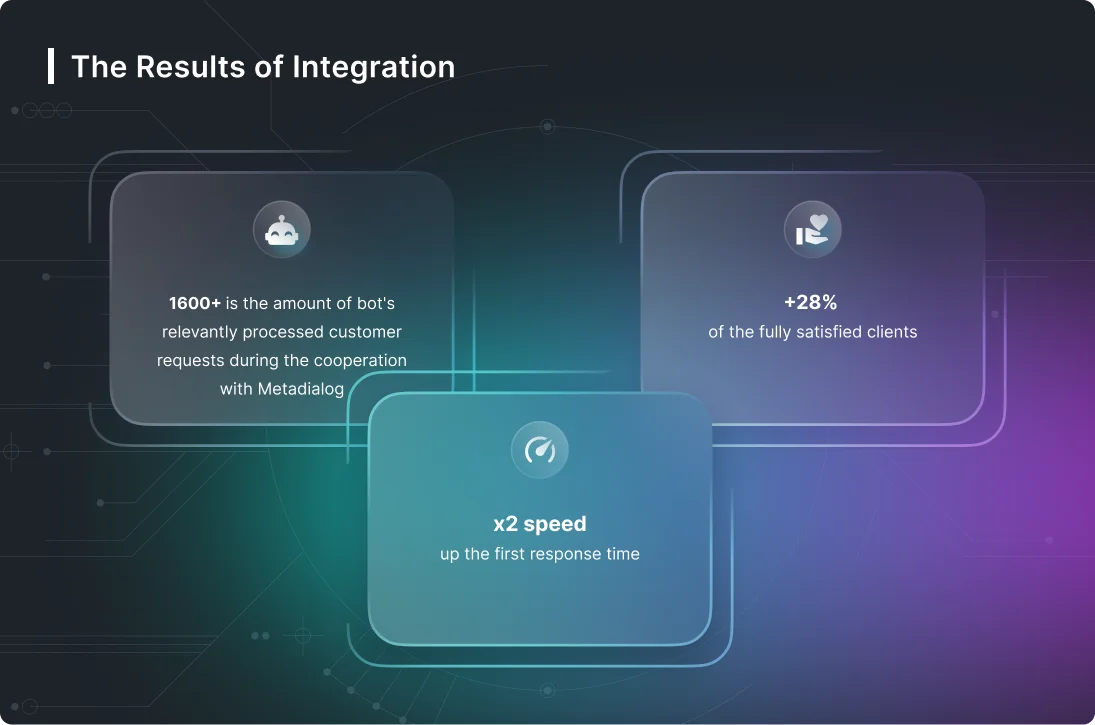

Read more about https://www.metadialog.com/ here.

Leave a Reply